The release of BDSA’s most recent wave of consumer research has offered insight into how consumer behaviour has evolved within the last six months, including consideration of the changes within Canada’s market as a result of the transition from Cannabis 1.0 to 2.0 and the impact of COVID-19.

Since Cannabis 2.0 products were introduced into the market, there has not been observed growth within Canada’s cannabis consumer population. Since BDSA’s last wave of the tracking study (fall 2019, pre-Cannabis 2.0), the proportions of cannabis consumers, cannabis acceptors (non-consumers who are open to cannabis use), and cannabis rejecters held steady at 35%, 28%, and 37%, respectively.

A notable difference has, however, been observed within consumer product choices. With the new availability of extract-based products such as edibles and topicals, the claimed average number of cannabis product categories used by consumers increased from 1.5 to 1.6. Consumption of these newer products has also grown, with edible consumption increasing significantly, from 50% to 57% and topicals growing from 23% to 26%. By comparison, claimed usage of inhalables was flat.

Product preferences have also grown since Cannabis 2.0, with the percent of consumers reporting a preference for edibles increasing by 3 percentage points (27% to 30%).

Consumers Adjusting Purchase Channels

As predicted by many, the growth of Canada’s legal cannabis market has resulted in a modest, 2% growth towards purchases within legal retail stores. Delivery service purchasing has also experienced a rise, likely as a result of both Cannabis 2.0 and the emergency orders allowing delivery during the COVID-19 pandemic.

Claimed acquisition of cannabis from friends or family members has also declined.

The shift in purchase channels is especially pronounced within BC, the heart of Canada’s legacy market. Consumers reporting cannabis purchases from a delivery service increased significantly, from 6% to 13% with reported acquisition from friends or family members declining significantly, from 44% to 37%.

Impact of COVID-19

BDSA’s recent research confirms that across North America, COVID-19 has impacted both shopping and consumption habits. While these impacts are evident in greater effect within the United States, impacts within Canada are still notable.

In total, 47% of Canadian consumers say they have not made changes to their cannabis shopping trip frequency, but just under one in five say their shopping frequency has increased due to COVID-19. A roughly equal number of consumers say their shopping has declined or stopped altogether. Top reported reasons for consumption include relaxation and relief from stress and anxiety.

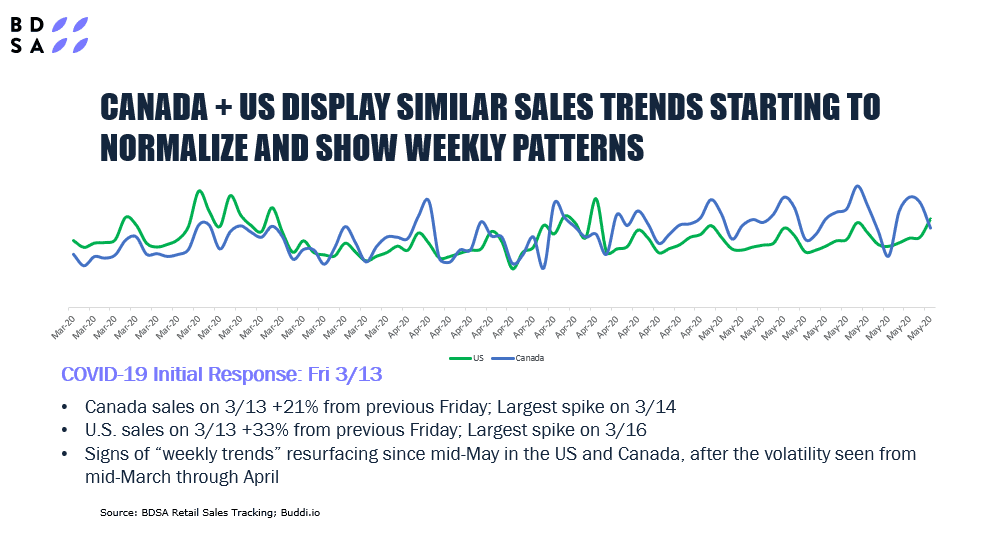

Research into both US and Canadian retail sales indicate that despite the ongoing pandemic, a return to normalized pre-coronavirus sales trends is developing.

Additional market insights into the Canadian cannabis retail landscape will soon be available with the release of retail sales tracking for Alberta and BC. Stay up-to-date with BDSA product releases at BDSA.com.