Although BDSA’s trending Consumer Insights shows greater penetration for cannabis beverages in the US compared to Canada, cannabinoid-infused beverages are already making waves in Canada’s edibles market. The innovation and initiative of the initial round of Canadian beverage brands in 2020 created a breakout year for cannabinoid-infused beverage sales across provinces.

While edibles were delayed until Cannabis 2.0, consumers have already developed a taste for edible products (yes, BDSA categorizes beverages under edibles). BDSA identifies approximately 30% of Canadian consumers preferring edible products mid-way through 2020. This is up significantly from preference seen pre-Cannabis 2.0. Canadian consumer preference for edibles is approaching levels seen among consumers in fully legal (and more mature with full product assortment) adult-use markets in the US.

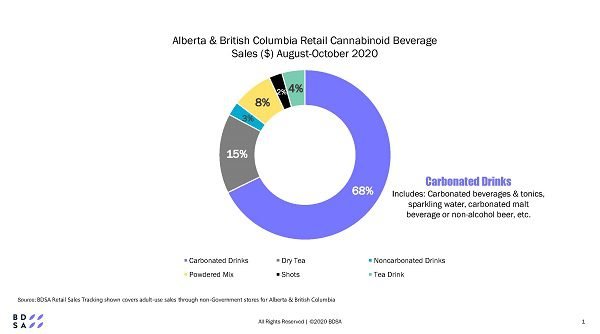

Carbonated drinks are really dominating the space, likely on account of availability. This segment is a key focus for many organizations, especially those that are supported by larger beverage manufacturers.

Fast Growth

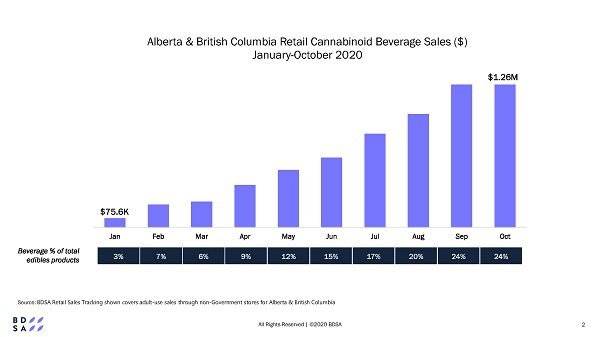

Keep in mind that the Canadian edibles market is still in its early stages of development. As of October 2020, the Canadian market had far fewer beverage products than most US markets, with about 35 beverage products in Alberta and British Columbia compared to over 240 beverage products in California alone. However, cannabinoid-infused beverages in Canada have seen some of the fastest growth of any edibles category in 2020, as seen in BDSA’s product-level retail sales tracking data. In Alberta and British Columbia alone, beverages grew from 3% of monthly edible sales in January 2020 to 23% of monthly edible sales by the end of October. Some of the fastest growth was seen from July to September, when beverage sales were seeing 20-30% month-over-month sales increases. Not surprising, availability of the products in stores is a major driver, as this spike in sales closely followed big beverage brands hitting store shelves in June and July.

This impressive first year of beverage sales in Canada definitely looks different than what has transpired in the fully adult-use legal US markets. As a comparison point, in the most successful cannabinoid-infused beverage market in the US today, BDSA tracks beverages at only 7% of total edible sales. The US beverage market has followed an interesting path over the past seven years, overcoming questionable consumer/product fit, confusing dosing mechanisms, some not so great tasting products, only high THC products available, and more.

Reasons for Purchase

To date, there are quite a few unique market dynamics for cannabinoid-infused beverages in Canada—a similar timeline for all edibles entering the market and arguably more thoughtful product formats, flavour, and branding than what was seen in the early days in the US. Another fact we cannot ignore, which has been discussed many times by BDSA, is the familiar form factor that draws in consumers who might be less knowledgeable about cannabis. Consumers are used to seeking functional benefits from beverages (relax, calm, energize, sleep, etc.), and cannabinoids fit right into these occasions. Canadian cannabis consumers are already claiming to seek the benefits of relaxation, peacefulness, fun, sleep, and pain management from cannabinoid-infused beverages. This creates substantial opportunity for beverage brands to take advantage of many different need states and occasions.

Lower-Dose Products Popular

In the US and Canada, beverages are proving to be well suited as a lower-dose product, which is notable as Canada’s regulations mandate that edible products contain no more than 10 mg of THC per package. Even in California, where state regulations limit THC to 100 mg per package for most edible products, beverages with 10 mg THC or less made up +50% of unit sales in 2020. By contrast, candy products with 10 mg THC or less represented only ~10% of unit sales in California this year.

This dynamic of beverages performing well as lower-dose products may play even stronger in Canada, given Canadian consumer preferences for THC dosage. While about 40% of cannabis consumers in US adult-use legal states report their ideal THC dosage is 10 mg or less, about 50% of Canadian cannabis consumers are looking for lower dosages. As edibles increase in availability in Canada, this preference for lower-THC products could further drive the strong position beverages is starting to carve out in the Canadian market.

Product Assortment & Availability

Look for savvy beverage brands to take advantage of the new demand for edible products, as well as leveraging their partnerships with large manufacturers on both sides of the US-Canadian border.

BDSA anticipates continued growth of the edibles market in Canada with increased assortment and availability, and beverages will be a substantial player. By 2025, BDSA forecasts the size of the Canadian edibles market to be 3-times what it is today, representing approximately 8% of total dollar sales. It is too early to tell exactly what portion beverages will own of this share in 2025, but the past 12 months (especially the past three months) show the beginnings of a fun and dynamic category to watch. Whether it be time to market, consumer/product fit, dosage, flavours, mg content, big beverage players, or all of the above, the Canadian cannabis-infused beverage market is just getting started.

Brendan Chesebro is an experienced analyst with industry-leader BDSA, delivering actionable insights on the world’s rapidly developing cannabis markets. Kelly Nielsen leads BDSA’s Insights & Analytics, and brings 13+ years of experience consulting on consumer goods, beverages, and most recently cannabis.