After the implementation of Canada’s Marihuana for Medical Purposes Regulations in June 2013, Alberta’s medical cannabis market saw some of the fastest growth of any Canadian province. Since the transition to an adult-use market in late 2018, Alberta has continued to show promise and represents one of the greatest opportunities for growth and development in Canada.

Meanwhile, Colorado is among the most mature cannabis markets in the US. It has been developing for over 20 years, first as a caregiver-based medical program, before the industry was fully regulated in 2011, then as the first market in North America to transition to adult-use sales in 2014. Though the path to a legal market has been vastly different between Alberta and Colorado, both markets have enthusiastic consumer bases that make them very appealing for industry development.

Here BDSA highlights a few key notes of comparison between the two markets, and how one can learn from what has transpired in Colorado and other established markets to understand the potential impact to Alberta in the future:

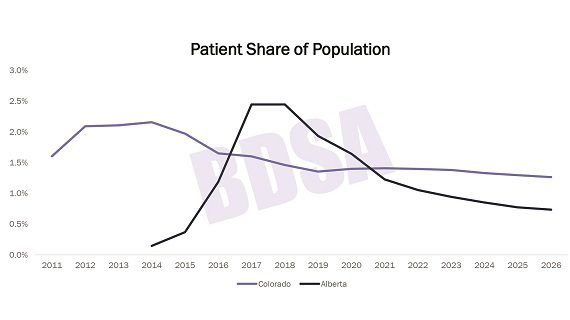

Both markets have seen strong medical markets due to high patient counts

Prior to the launch of adult-use sales, medical patients in both markets represented more than 2% of the population. Alberta’s patient share of population peaked at 2.45% in 2018, with the number of patients passing 110,000 prior to the launch of adult-use sales in October of that year.

While Alberta is not expected to have patient retention as strong as Colorado’s in the long run, patient counts are still high enough to maintain a considerable medical market. While patient numbers have fallen considerably since the start of adult-use sales, Alberta is still home to almost 20% of Canada’s registered patients despite making up only 11.6% of the total adult population.

According to BDSA’s market forecast, medical sales are still expected to bring in over $70 million in 2021, then fall gradually to about $38 million by 2026.

Alberta’s shifting consumer attitudes suggest strong growth on the horizon

BDSA’s Consumer Insights suggests that there is room for the expansion of the consumer base in Alberta. According to consumer surveys from Fall 2020, 39% of Albertan adults report consuming cannabis in the past 6 months, while 33% identify as non-consumers who are open to cannabis, and the remaining 29% indicate that they are not open to cannabis consumption.

This mix of consumer and non-consumer attitudes parallels those of Coloradans surveyed in the Spring of 2019, roughly five years after the launch of adult-use sales. At this time, 42% of adults identified as consumers and 30% rejected cannabis consumption in Colorado. However, by the Fall of 2020, the consumer penetration had grown substantially to nearly half of the adult population, while rejecters had shrunk to just 23%.

This sizable growth in Colorado, occurring more than 6 years after the launch of adult-use sales, indicates the potential for Alberta’s consumer share to expand considerably as its adult-use market matures. From March 2019 to March 2021, monthly sales in Colorado grew from roughly $145 million to almost $200 million, illustrating the degree to which an expanded consumer base can drive growth even in well-developed legal markets.

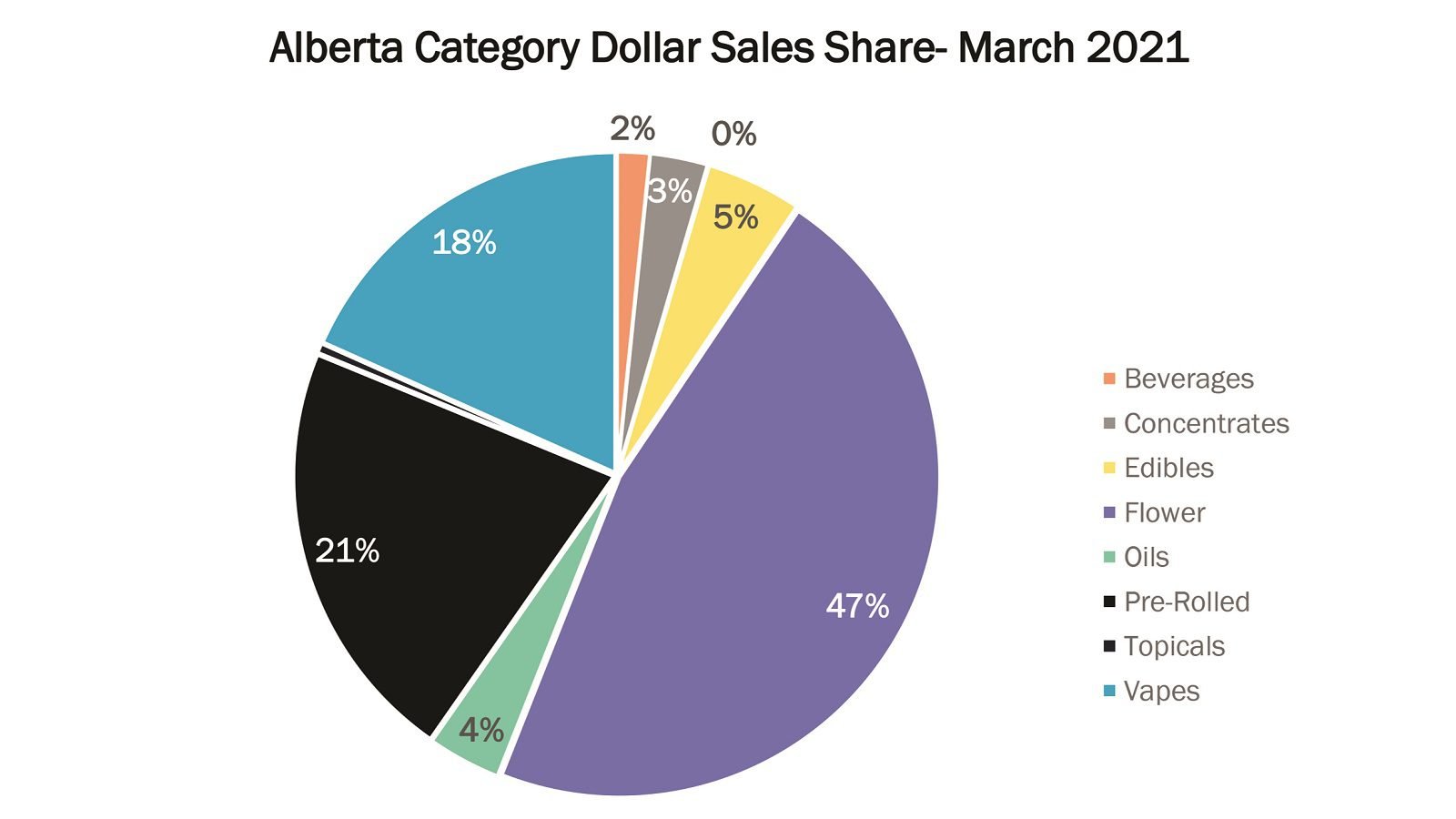

Flower and pre-rolled sales remain strong in Alberta, but vapes and edibles are picking up steam

Since the launch of Cannabis 2.0 products in October 2019, the product mix in Alberta has begun to shift more closely to that of most US markets, with flower maintaining a large share of category sales and vapes seeing rapid sales growth.

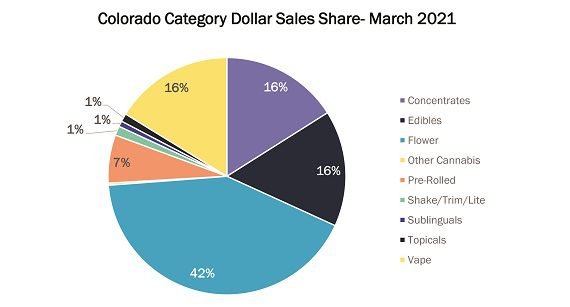

Flower’s share of monthly sales in Alberta fell from 52% in May 2020, to 47% in March 2021 according to HiFyre Retail Sales tracking. Contrastingly, pre-rolled joints have gained share of total sales since the introduction of new products. Sales of pre-rolls are much stronger than in Colorado, where pre-rolls accounted for 7% of monthly sales in March 2021.

Of the products that were introduced with Cannabis 2.0, vapes have performed the strongest, with vapes’ share of Alberta sales totalling 18% in March 2021. Non-vape concentrates have seen more sluggish growth in most Canadian markets, and Alberta is no exception, with the category making up just 3% of total sales in March 2021. Edibles share remained mostly flat from May 2020, totalling just over 5% of March 2021 sales, which is still substantially lower than nearly all US legal markets.

By contrast, dabbable concentrates perform much better in Colorado compared to other US markets and Alberta. In March 2021, dabbable concentrates and vapes both held a 16% share of legal sales in Colorado.

So what is next?

Alberta’s market has seen considerable growth since the launch of adult-use sales, with legal sales totaling almost $600 million in 2020, up from $415 million from 2019. As the consumer base expands and the adult-use market matures, legal sales are expected to grow to total over $1.2 billion by 2026.

Alberta’s market has seen considerable growth since the launch of adult-use sales, with legal sales totalling almost $600 million in 2020, up from $415 million from 2019. As the consumer base expands and the adult-use market matures, legal sales are expected to grow to total over $1.2 billion by 2026.