Cannabis retailers operating in multiple provinces face a unique challenge in the way both their businesses, and their cannabis products themselves, are taxed differently across Canada.

Unlike alcohol, where taxes on specific products may vary from province to province but are generally in the same range, cannabis taxes can vary radically between provinces. The wide variety of wholesale markup is illustrated with the comparison chart, which was created to complement a research report on this subject authored by Michael J Armstrong. Even alcohol faces challenges from the provincial tax variance, which has led to a booming, but technically illegal, online interprovincial wine trade. It is not hard to imagine how much worse the problem would be if alcohol were subject to the same tax variance as cannabis.

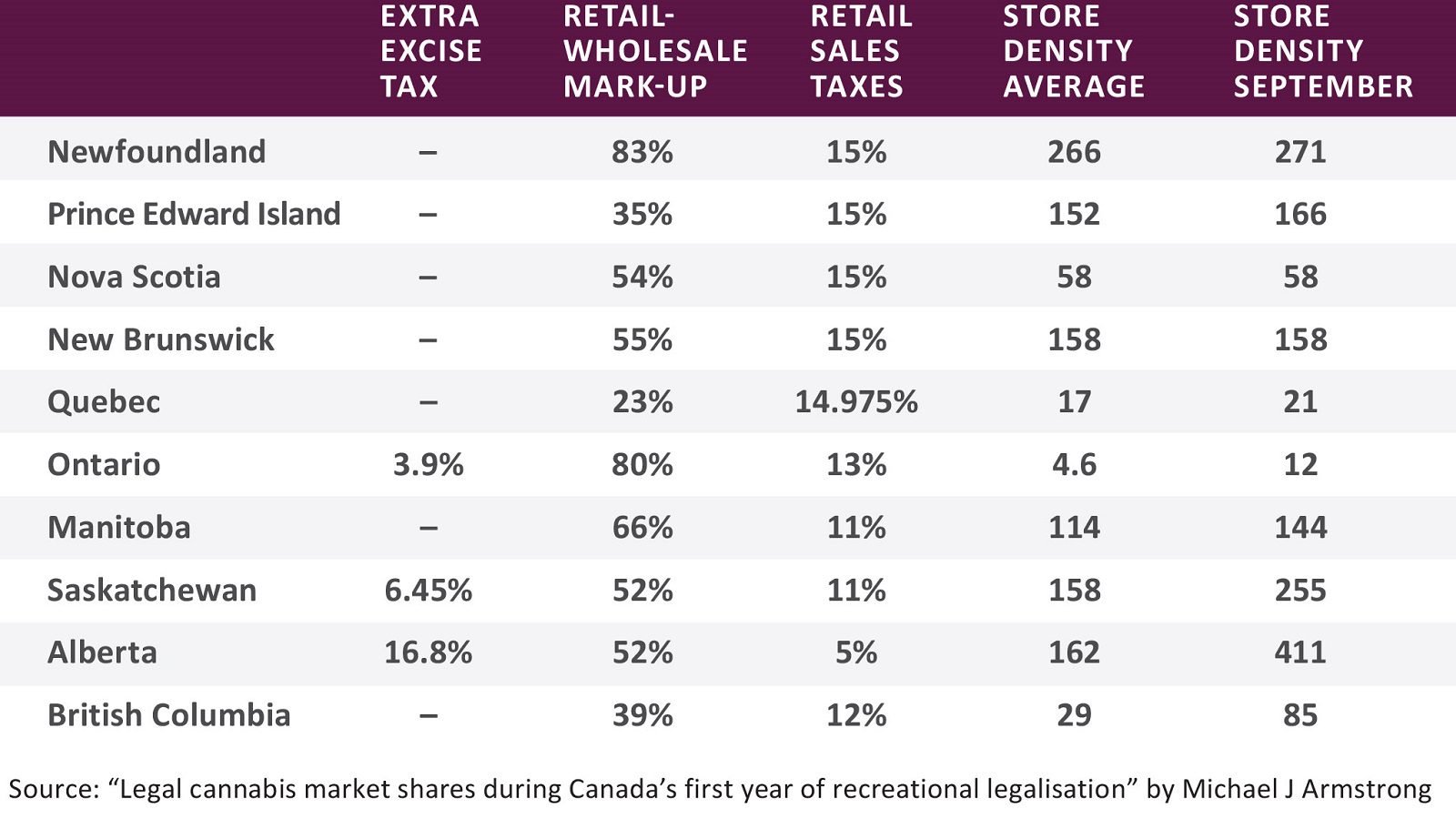

In Armstrong’s report “Legal cannabis market shares during Canada’s first year of recreational legalisation” he describes, “The first three columns show each province’s extra ad valorum excise tax (if any), its estimated combined retail-wholesale price mark-up, and its combined federal-provincial sales tax rate. The last two columns show the store density (in stores per million users), first averaged across all 12 months and then just for September 2019.”

This uneven provincial cannabis tax regime results in significant variance in the retail cost of identical products in different provinces. As an example, a half gram vape cartridge sold in Ontario for $30 costs as much over $37 in British Columbia, a difference of 20%. Alberta retailers carry a combined wholesale markup of 68.8%, which includes a 16.8% additional excise burden that retailers need to absorb in that province.

This variance in product taxation is compounded by varying tax and regulatory burdens at the municipal level, which can have a significant bottom line cost on retailers, and that must also be passed on to consumers.

For example, stores in Vancouver face a $35,000 annual business licensing fee and several months, even years, of regulatory work is required before opening, while stores in other municipalities in the Lower Mainland can pay as little as a few thousand dollars a year and are granted retail licenses in a matter of weeks.

These variations make it very difficult for retailers with intentions to operate in multiple jurisdictions, as their expansion and site acquisition plans are subject to significant and varying challenges; once open, they also find it difficult to take advantage of economies of scale due to varying taxation.

It is also important to note the impact that these tax differences have on licensed producers that are faced with a landscape where the final retail price consumers pay for their product not only varies significantly from province to province, but even from city to city or shop to shop. With little to no control over how these prices are set, producers are left with very few tools to build market share or compete with the black market.

While government at all levels are in agreement about the importance of giving provinces and local governments a significant say in where and how cannabis is sold, it is equally important that all jurisdictions are working to bring their regulations into harmony, and base them on the best model available.

Provinces and the federal government should work together with municipalities on a coordinated set of best practices for cannabis taxation and regulation, based on the principals of promoting adoption of the legal system in order to maximize tax and public health benefits. This would leave local and provincial governments free to continue regulating locally, while reducing the more negative effects of regulatory differences.

Without this kind of harmonization, cannabis retailers will continue to face a significant uphill challenge in their battle to take market share from unregulated retailers, which often fill the gaps in regulations by offering a cheaper or more convenient service.

Jaclynn Pehota is on the Advisory Board of the Association of Canadian Cannabis Retailers (ACCRES) and can be reached at jaclynn@accres.ca.