Leading up to October 2019 and the legalization of Cannabis 2.0 products, there was a great deal of excitement and investment from large alcohol manufacturers in the cannabis space. Despite initial predictions and investment, cannabis-infused beverages make up only 2.1% of the total Canadian market as of December 2021. In the United States, cannabis beverages reached 1.1% of the total market in January 2022.

Headset argues beverages are performing successfully as a cannabis product category in both Canada and the United States. In their March 2022 report, Headset dives deep into the category, exploring growth in cannabis beverages over the past two years in Canada and the United States by examining market share, growth in new products, package sizes, top brands, and more.

Note: Headset’s report examines markets in Arizona, Colorado, California, Illinois, Massachusetts, Washington, Nevada, Oregon, and Michigan in the US and Alberta, Ontario, British Columbia, and Saskatchewan in Canada.

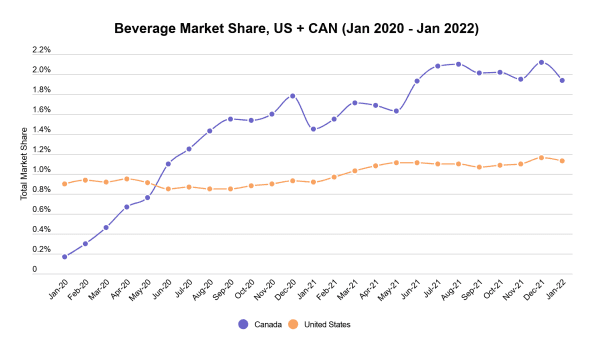

Market Share of Cannabis Beverages

Market Share of Cannabis Beverages

Market Share of Cannabis Beverages

Market Share of Cannabis BeveragesSales of cannabis beverages were introduced along with other Cannabis 2.0 products in the Canadian market around January 2020. Consumers welcomed the introduction of this new form of consumption, with the beverage category increasing to 1.8% of the total market by December 2020.

Beverages continued to see significant growth in Canada throughout 2021. By the end of last year, the category reached peak market share at just over 2.1% in December. The US has seen slower, but more consistent growth in market share.

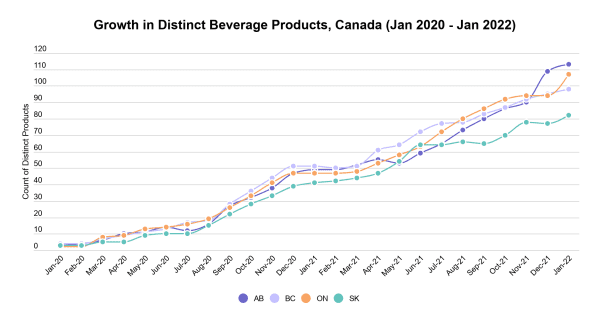

Growth in Cannabis Beverage Products in Canada

Growth in Cannabis Beverage Products in Canada

Growth in Cannabis Beverage Products in CanadaStarting in January 2020, there was a stable growth in distinct products throughout the first half of 2020. By October 2020, each market saw an accelerated pace of new beverage products sold within the market. In December 2021, Alberta had almost 110 distinct beverage products, the most of the four provinces shown.

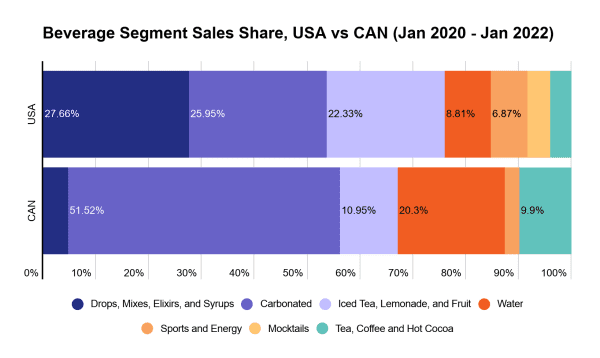

Beverage Segment Shares

Beverage Segment Shares

Beverage Segment SharesIn the US, drops, mixes, elixirs, and syrups make up 27.7% of total beverage sales from January 2020 to January 2022 – the largest beverage segment contribution, closely followed by carbonated beverages at 25.95% and iced tea, lemonade, and fruit beverages at 22.3%.

Comparatively, in Canada, drops, mixes, elixirs, and syrups only make up 4.7% of the beverage category, while carbonated beverages dominated – making up 51.5% of sales. The water segment is also strong in Canada, making up 20.3% of sales compared to 8.8% in the US.

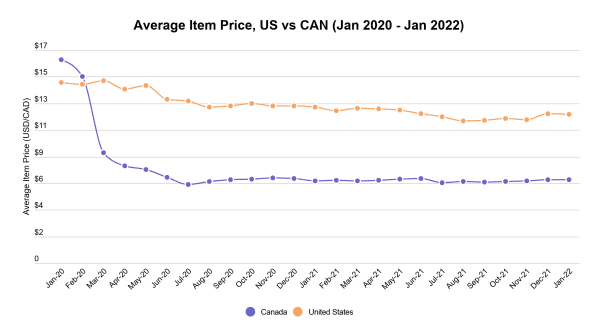

Prices of Cannabis Beverages

Prices of Cannabis Beverages

Prices of Cannabis BeveragesCanadian cannabis beverage products averaged $16.21 per product in January 2020. After a significant drop, the average item price (AIP) of beverages in Canada has hovered around $6 per product since July 2020. The US has experienced a slower, more consistent drop in AIP as new markets and products are introduced.

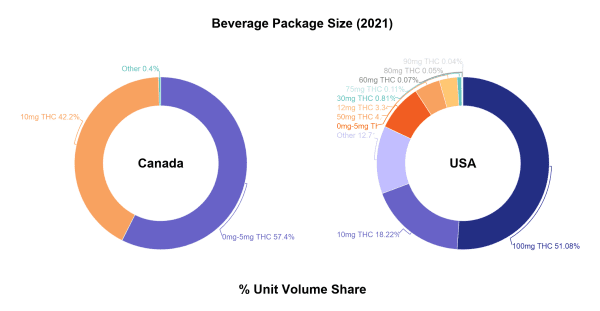

Package Sizes of Cannabis Beverages

Package Sizes of Cannabis Beverages

Package Sizes of Cannabis BeveragesProducts in the US are clearly different from those in Canada, mostly attributed to regulatory differences. In Canada, beverages cannot exceed more than 10mg of THC per package. In many US markets, the limit is 100mg.

In Canada, 57.4% of cannabis beverage products sold in 2021 contained between 0 and 5mg of THC. 42.4% of products contained 10mg of THC and a very small portion (0.4%) contained various among of THC.

Comparatively, in the US, 51.1% of beverage products sold contained 100mg of THC per package. The US also has greater variation in package size.

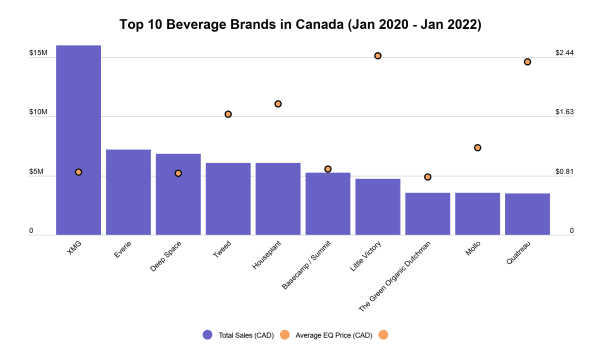

Top 10 Beverage Brands in Canada

Top 10 Beverage Brands in Canada

Top 10 Beverage Brands in CanadaThe leading cannabis beverage brand in Canada from January 2020 to January 2022 was XMG, posting nearly $16 million in sales. This is followed by Everie, with just over $7 million in sales.