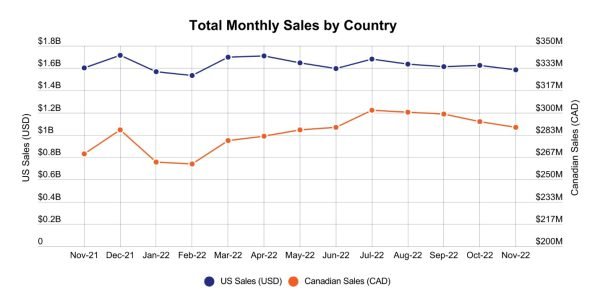

The Canadian cannabis market saw steady sales growth in 2022. As of November, sales are up 7% from a year ago.

As the year draws to a close, let’s take a look back at how sales trends have shifted over 2022. Headset‘s report will examine the broad changes among the most key cannabis sales metrics that we track here at Headset such as pricing trends, shifts in cannabis product categories, and demographic preferences.

Analyses include data from most or all of the following markets AZ, CA, CO, FL, IL, MA, MD, MI, NV, OR, and WA in the US and AB, ON, BC, SK in Canada.

Total monthly cannabis sales in the US and Canada

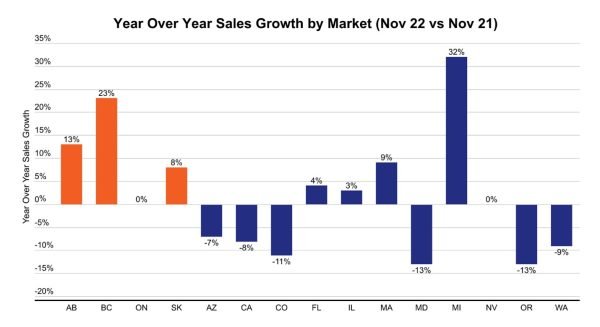

Sales growth in individual states and provinces

Not all markets performed in the same way over the past year. This graph shows the relative increase or decrease in total sales within each market, comparing November 2021 to November 2022. Most Canadian markets saw positive growth while Ontario, the largest province by population and total cannabis sales, was flat.

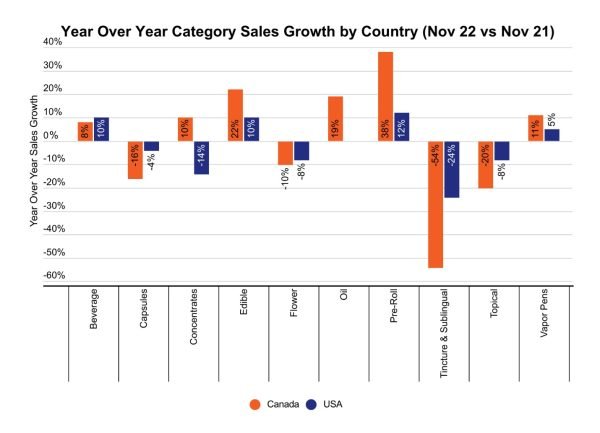

Category performance in the US and Canada

Next let’s look at which product categories performed the best over the past year. This graph compares the year over year sales growth of each product category within each national market. Immediately we can see that some categories performed better than others. Tinctures, Topicals, Capsules, and most significantly, Flower all saw year over year sales declines in both the US and Canada. Tinctures, Topicals, and Capsules all tend to fall within the ‘wellness’ use-case for customers. A broad-scale decline across these product types may hint at a shift towards more true recreational use and away from purchases motivated by symptom treatment. Flower was a category that surged in sales early in the pandemic and may still be correcting out of that ‘COVID-moment.’

Beverages, Edibles, Vapor Pens, and Pre-Rolls all saw positive year over year growth in both the US and Canada. This again potentially indicates a shift in consumer behaviour towards more portable and shareable product types.

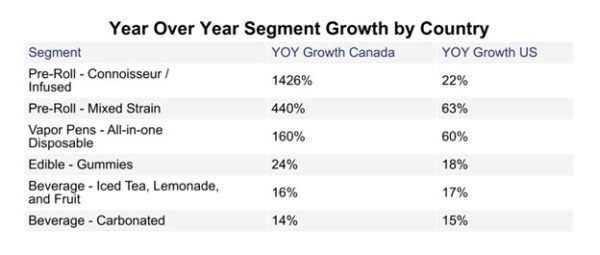

Segment performance in 2022

Both Infused and Mixed Strain Pre-Rolls have performed incredibly well in both the US and Canada in the past year. In both countries, the Connoisseur/Infused segment is now the second largest within the Pre-Roll category and appears to be on track to overtake Hybrid – Single Strain for the number one spot in the coming year.

All-in-one Disposable Vapor Pens have seen strong growth in both countries, again indicating more customer interest in portable product formats.

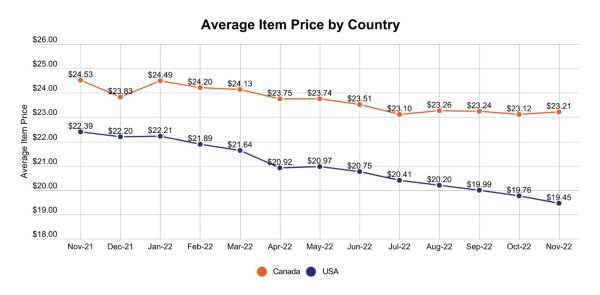

Changes in cannabis pricing in the US & Canada in 2022

Due to historically large increases in inflation, pricing has been a popular topic of conversation throughout the year. In the cannabis industry however, prices are moving in the opposite direction. This graph shows the market-wide average price of a cannabis product by month from November 2021 to November 2022. Prices in the US have been decreasing steadily, dropping -13% since November 2021. In Canada, the decrease in price has been less steady, but average item prices in November 2022 are 5% lower than in November 2021.

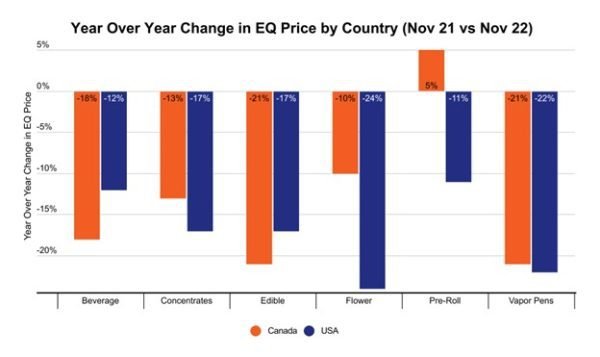

Change in EQ price by category in the US & Canada

Shifts in average item price can sometimes be hard to interpret since changes in consumer preferences towards larger or smaller package sizes could cause the metric to change.

Instead, we can use equivalized (EQ) price to normalize across all package sizes within each category. For Flower, average EQ price is calculated as the total sales divided by the total number of grams of Flower sold, which gives us the average price of a single gram of Flower, regardless of the package size it was sold in. This metric will better account for shifts in consumer preference between package sizes. For Concentrates, Flower, Pre-Roll, and Vapor Pen categories EQ price represents the average price per gram, while for the Beverage and Edible categories, EQ price represents the average price per milligram of THC.

Here we see that the Canadian Pre-Roll market was the only place where average EQ price rose over the past year. This can likely be explained by the surge in popularity of infused Pre-Rolls, which require more expensive ingredients and production methods. In all other major categories, average EQ prices saw significant declines in both the US and Canada. The average price per gram of Flower in the US declined by nearly a quarter from November 2021 to November 2022. These precipitous drops in price can likely be explained by a combination of decreased demand, over-supply, and increased competition.

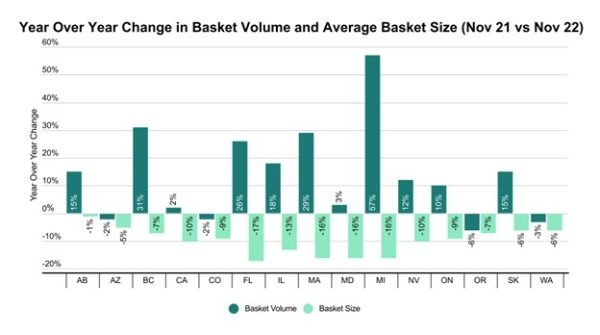

Cannabis basket trends in 2022

One of the best ways to understand how topline sales are changing is to look at basic basket metrics. Total sales can be described as the total number of transactions multiplied by the size of the average transaction. This graph shows us the year over year changes in both of these metrics within each US and Canadian cannabis market.

Average basket size has decreased in all markets. This means that customers are spending less per trip to a cannabis retailer now than they were one year ago. This can likely be attributed to the pricing compression we saw in the previous graphs. Customers are simply getting more for their money as prices decrease.

Changes in total basket volume, on the other hand, are not quite as consistent. Clearly, topline sales growth in the best-performing markets were primarily driven by increases in transaction volume.

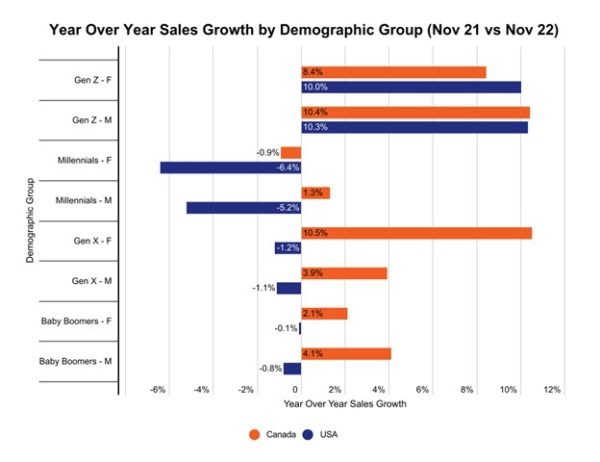

Demographic trends in the US & Canada

In this final graph, let’s take a close look at cannabis customers. This graph shows the year over year sales growth of different customer demographic groups, described by age group and gender. As always, the youngest customer cohort is growing the fastest. In both the US and Canada, sales to Gen Z customers grew significantly over the past year. In fact, in the US, Gen Z was the only age group that posted positive sales growth. Gen Z’s sales growth is always strong as this is the only age group with new customers aging into the market each day by turning 21 in the US and 19 in Canada.

An interesting standout in this analysis is the growth of sales to Canadian Female Generation X customers. This cohort had the strongest growth of any in Canada, besting even Gen Z Male customers by one tenth of a percentage point. Canadian operators should continue to watch this trend as a previously untapped customer segment may be emerging.

Conclusion

A lot has changed in the industry over the past year. While cannabis sales in general have slowed down, Canadian markets continue to see positive sales growth and trends in product categories and pricing are shifting constantly.