Capsules, Tinctures & Sublinguals, and Oils (CTSO) only make up 1% of the combined market share for Canada and the United States, but the Capsule category is growing. A recent Headset report compares emerging trends, market share, and prices for each of these categories in Canada and the United States. Here are the highlights.

Note: data is from January 2020 to December 2021 unless otherwise noted. As Canadian operators are unable to infuse alcohol products, Headset examined the Oil category for Canada and Tinctures & Sublinguals in the US.

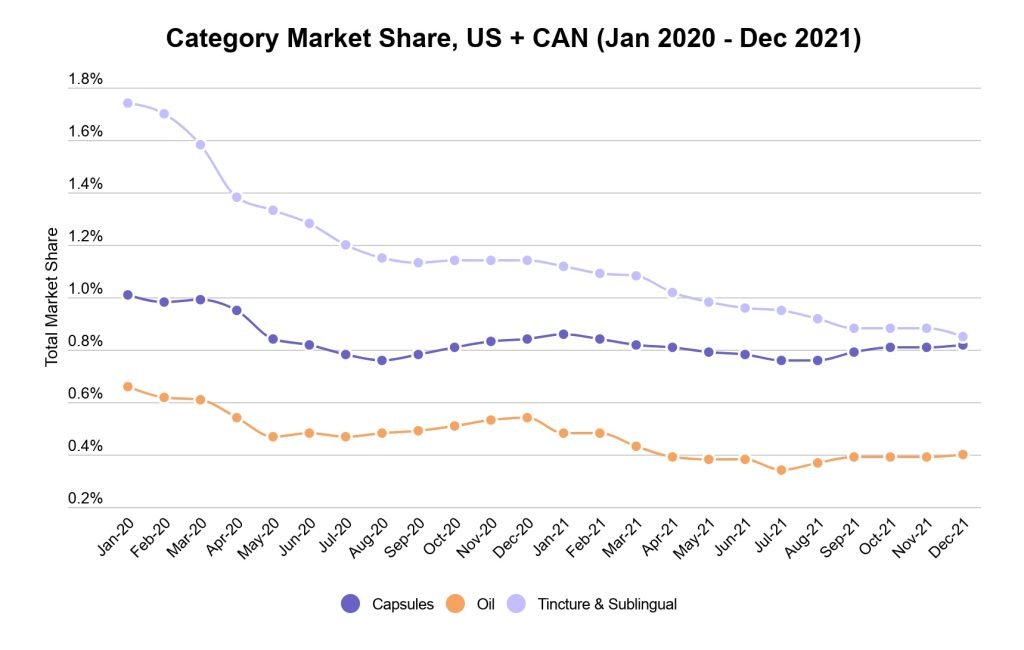

Category Market Share in the US and Canada

Category Market Share in the US and Canada

Category Market Share in the US and Canada

Category Market Share in the US and CanadaMarket share for all categories has dropped since January 2020. Tinctures & Sublinguals experienced the largest decrease, dropping from 1.74% to 0.85%. Capsules dropped slightly but has been trending up towards the end of 2021.

Oil has grown in popularity over the last few years, but it remains the smallest contributor to the market, as it is tracked in Canada only. Market share decreased slightly from 0.66% to 0.4% across the two years.

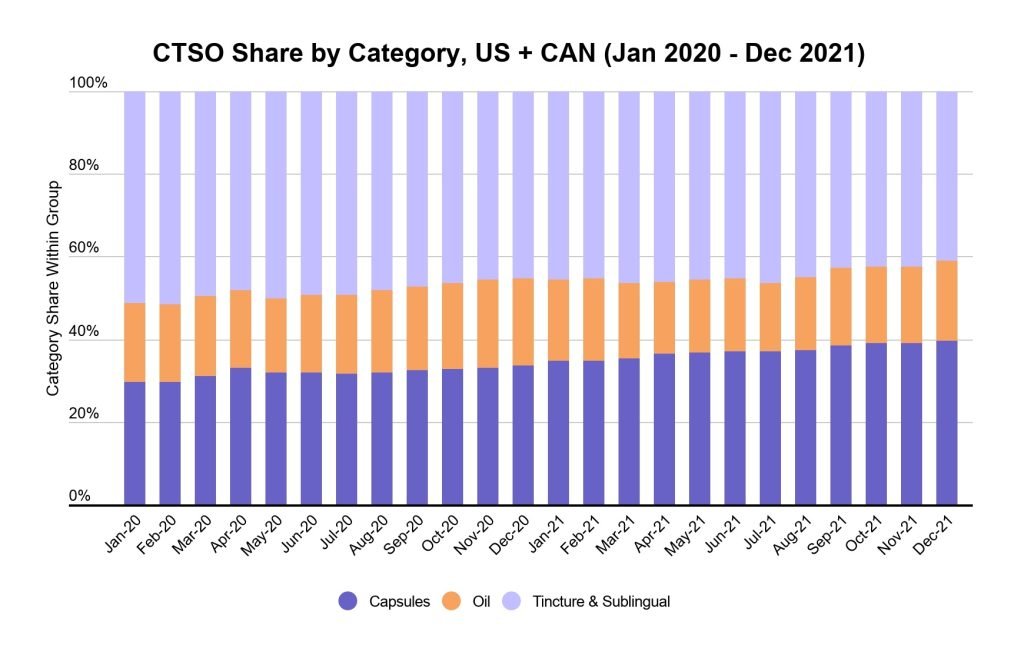

Category Share within the CTSO Group

Category Share within the CTSO Group

Category Share within the CTSO GroupWithin the total market share of these combined categories in the US and Canada, Capsules are the only category to experience growth, increasing almost 10%. Oils have remained mostly constant, while Tinctures & Sublinguals had the largest drop in share, decreasing from 51% to 41%.

A 2021 Deloitte report that explored growth opportunities within existing cannabis customers suggested a shift to using cannabis for general wellness has increased interest in capsules, but more people were interested in capsules, topicals, and beverages than actually bought them.

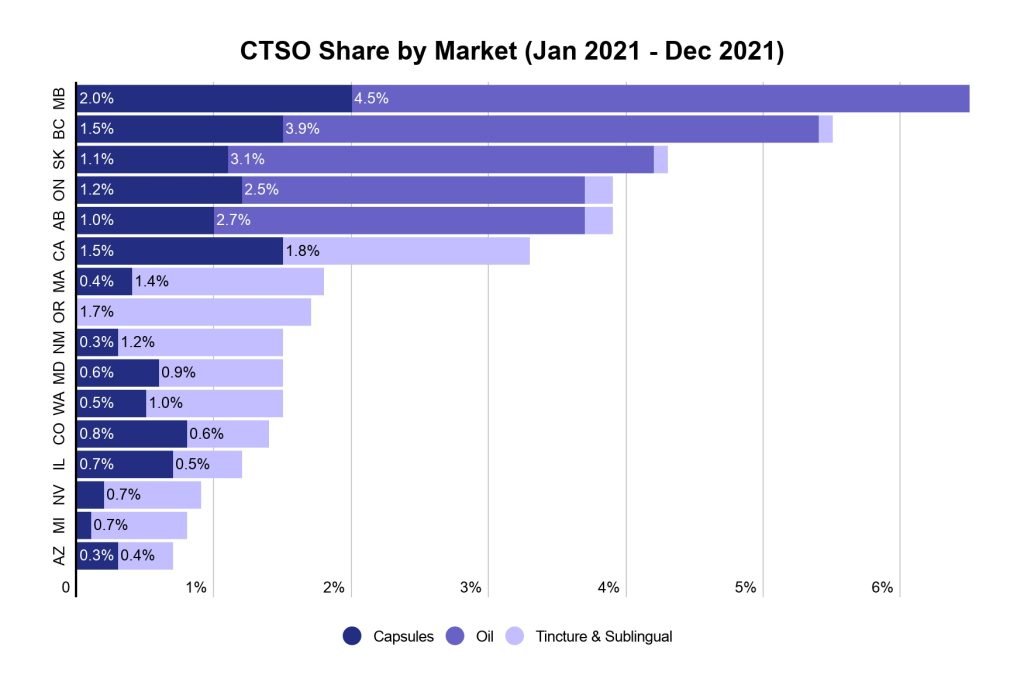

Market Share in Provinces in 2021

Market Share in Provinces in 2021

Market Share in Provinces in 2021Capsules and oils perform well in Canadian provinces, with Manitoba, British Columbia, Saskatchewan, Ontario, and Alberta leading combined market share in 2021. Despite Capsule category growth, Oils have double the market share of capsule products.

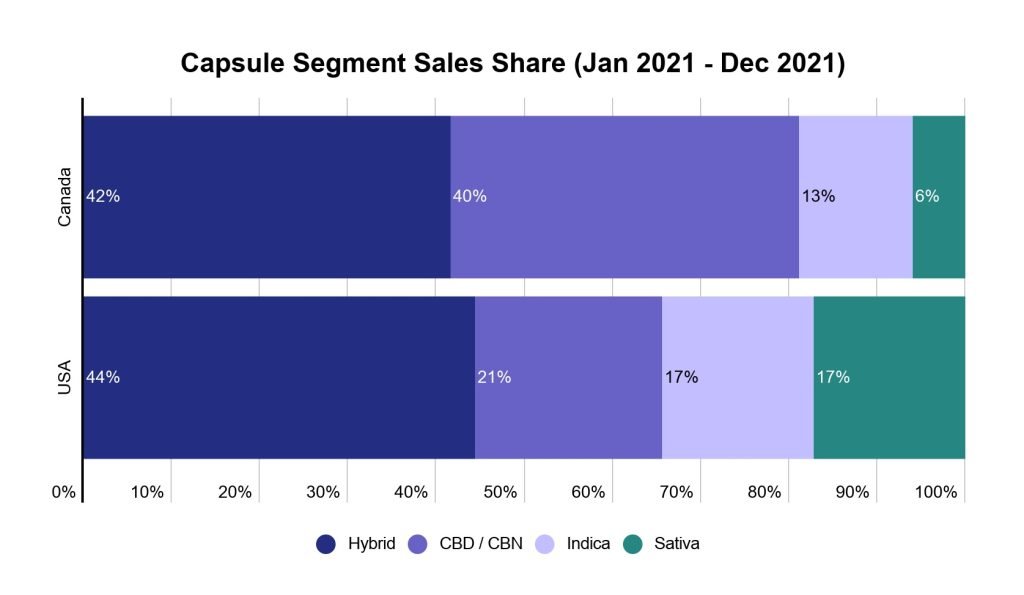

Cannabis Capsule Sales

Cannabis Capsule Sales

Cannabis Capsule SalesMost Canadians are buying Hybrid or CBD/CBN products, with these segments making up over 80% of total capsule sales in Canada.

In the US, Indica and Sativa designated segments are more popular.

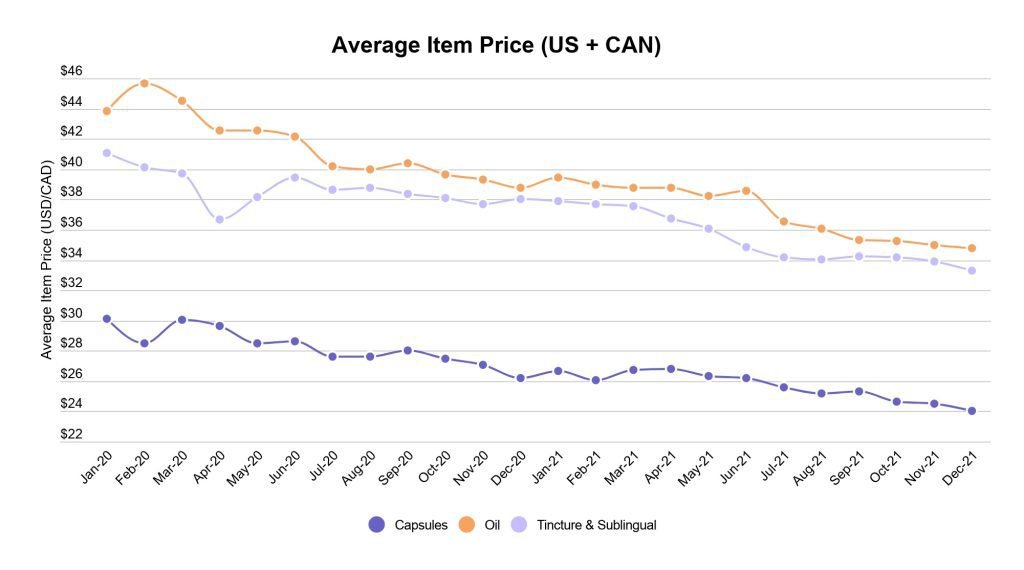

Prices of Capsules, Tinctures & Sublinguals, and Oils

Prices of Capsules, Tinctures & Sublinguals, and Oils

Prices of Capsules, Tinctures & Sublinguals, and OilsThe average item price for all three categories has steadily declined over two years, dropping by around 20%. The Oil category’s AIP started at $42.83 per unit in January 2020 and dropped to $34.78 per unit in December 2021. Tinctures & Sublinguals and Oils saw similar drops.

Top Brands

The top cannabis Capsule brands in Canada are: Redecan, Tweed, Daily Special, Mood Ring, and Dosecann. From January to December 2021, consumers spent a collective $14 million on Redecan brand capsules. The top cannabis Oil brands in Canada are: Redecan, MediPharm Labs, Solei, Pure Sunfarms, and Tweed. Redecan had $26.7 million in annual Oil sales in 2021.

What’s Next

Since the early days of legalization, cannabis derivatives have been expected to dominate the market. Headset suggests it is only up from here. With new products, advanced formulations, and emerging brands, we can expect to see plenty of opportunities for the Capsules, Tinctures & Sublinguals, and Oils market to grow and develop.