Millennial and Generation Z consumers account for the majority of cannabis sales in Canada and the United States according to a new report by Headset.

Gen Z represents the fastest-growing consumer group in both Canada and the US, largely stemming from their growth and maturation. Millennials remain the number one cannabis consumer, capturing almost half of the market across North America.

In the report, Headset explores cannabis consumer demographics in 2023, breaking down gender, age, and geography of cannabis sales in the US and Canada. The report covers select cannabis markets in the United States (Nevada, Massachusetts, Colorado, California, Washington, Oregon, Michigan, and Arizona) and Canada (Alberta and Ontario).

Gender

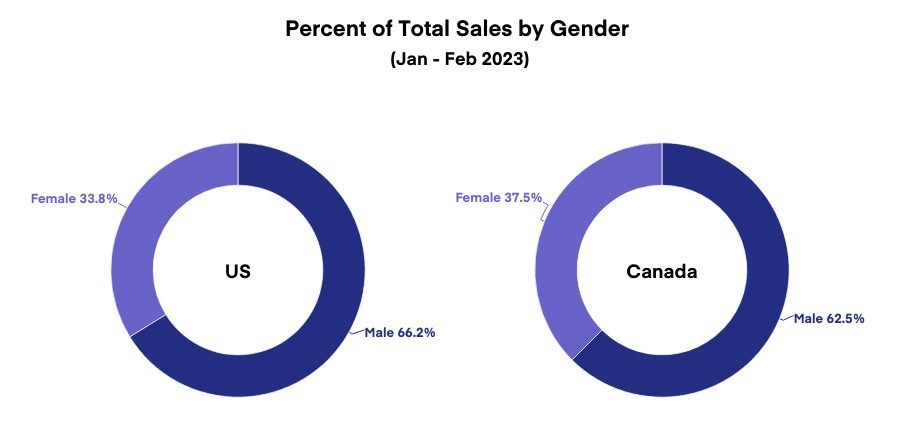

In the US and Canada, males account for about two-thirds of all cannabis sales, while females capture the remainder. In Canada, there is a higher representation of females (37.5%) among cannabis consumers than in the US (33.8%).

Since January 2021, females have seen a slight, but inconsistent increase in their percentage of total sales, with growth rates between January 2021 and December 2022 equal to 1.2% in Canada and 0.27% in the US.

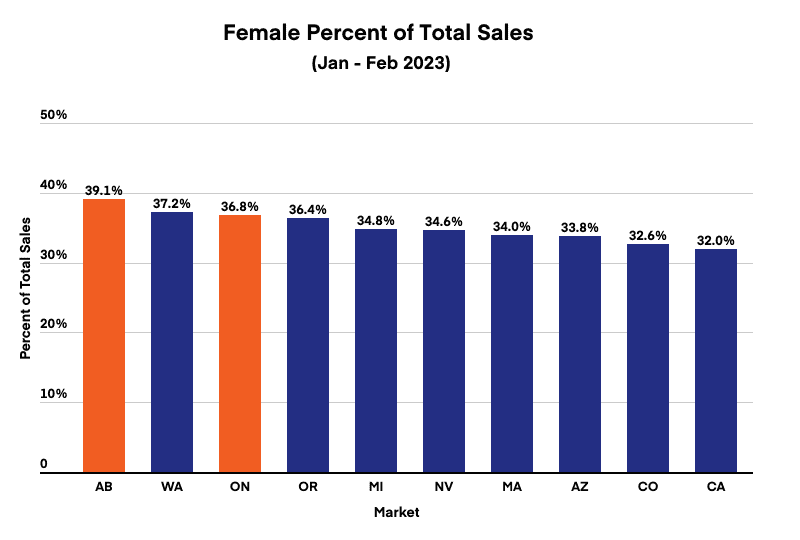

Alberta and Ontario captured the first and third highest female percentage of total sales at 39.1% and 36.8% respectively.

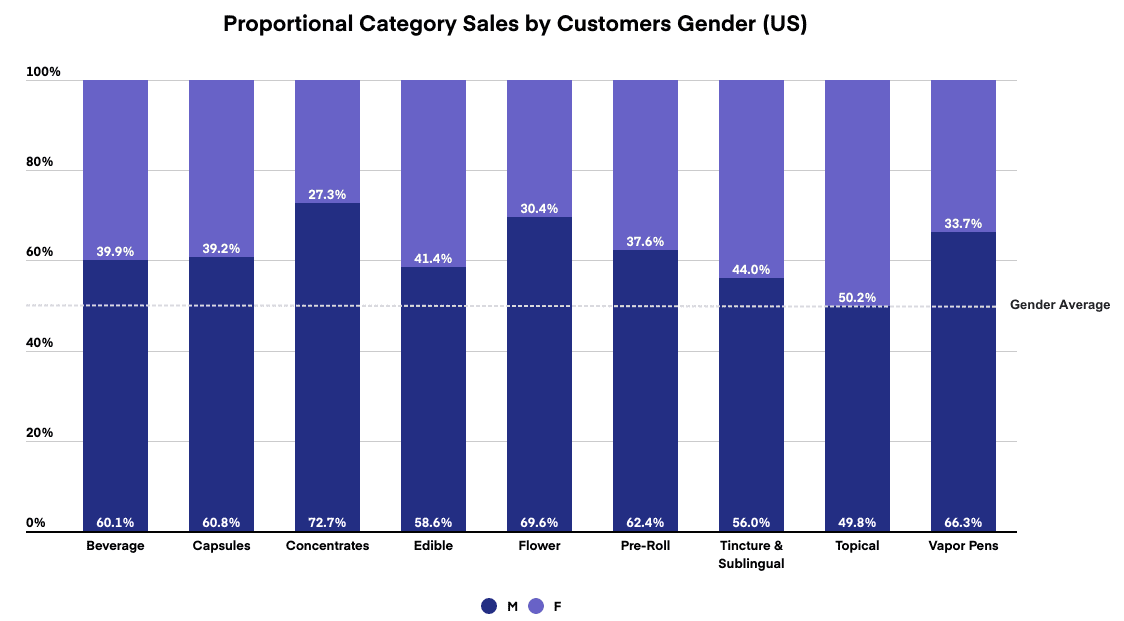

Several categories skew heavily towards female consumers, including topicals and tinctures and sublinguals, while male consumers dominate concentrates and flower sales.

Age Group

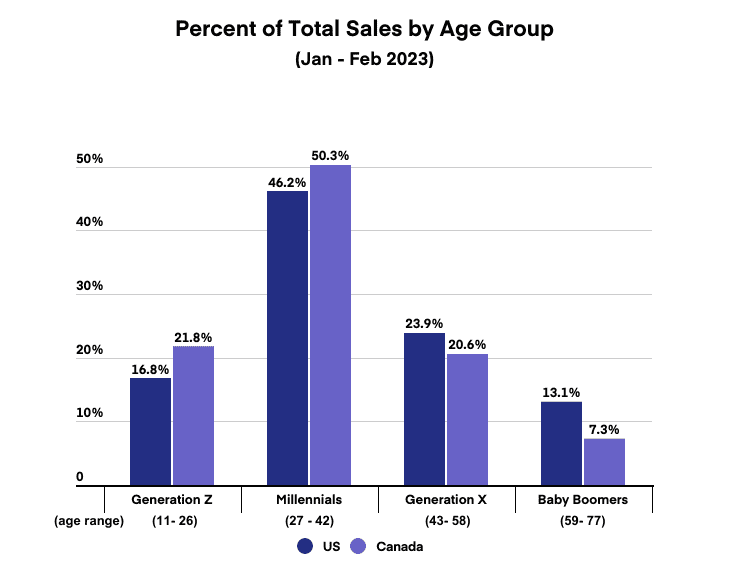

Millennials capture nearly half of every dollar spent on cannabis in Canada and the US. Millennials and Gen Z consumers account for 72.1% of all tracked sales in Canada, versus 63% in the US. This is heavily influenced by the legal age of consumption, which is 18 or 19 in Canada and 21 in the US.

Gen Z is the fastest-growing group of consumers. In Canada, their total share of sales has increased steadily from 17.5% in Q1 2021 to 21.5% in Q4 2022, while other groups have remained consistent or decreased in the case of millennials.

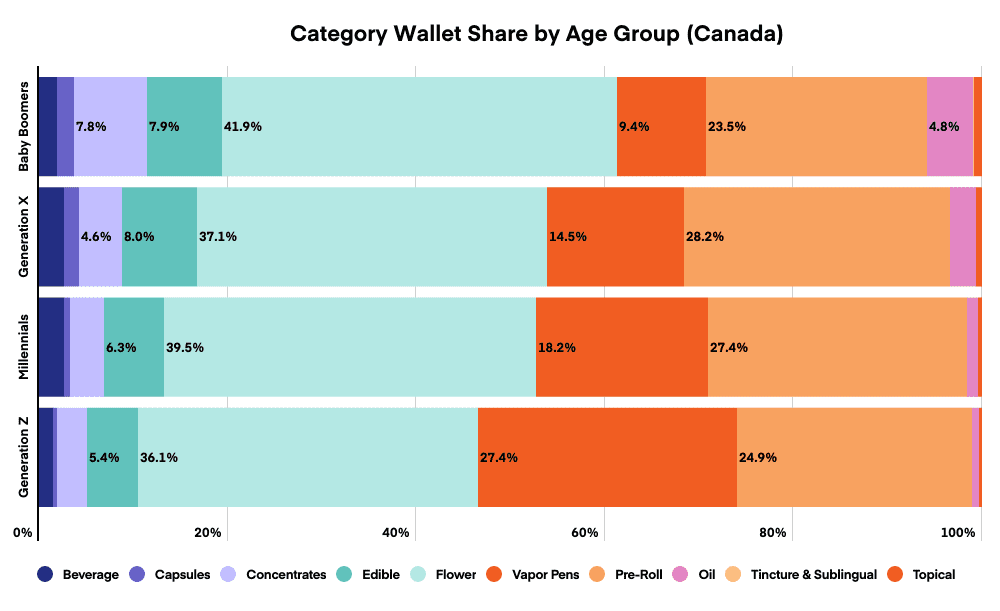

With respect to category wallet share by age group, mature product categories such as flower and edibles, skew older, while newer categories such as vapor pens skew younger. Pre-rolls are preferred by millennials and Gen X, capturing between 27% to 29% of wallet share.

Basket Size

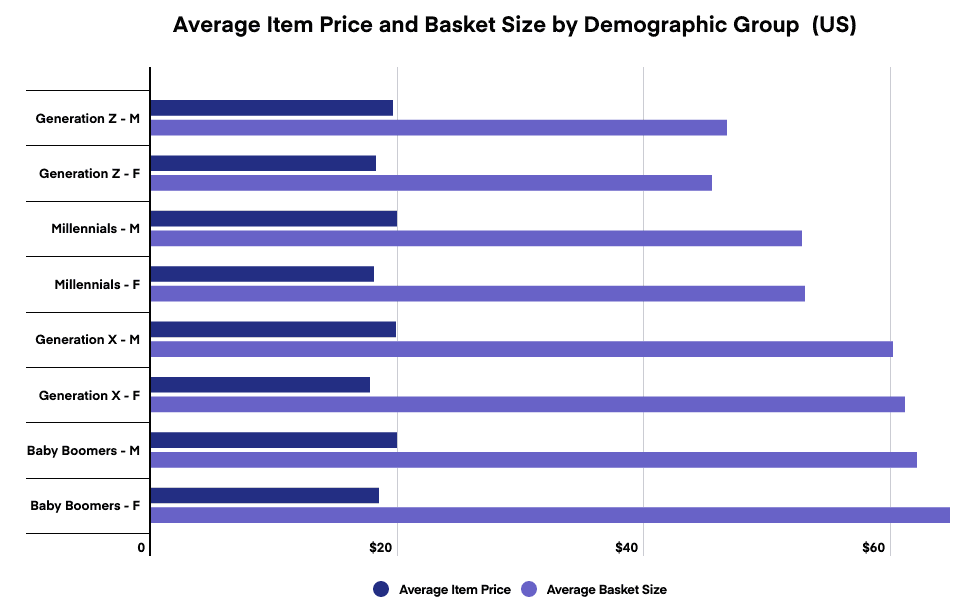

Across age groups, average item price stays fairly constant, but male consumers tend to purchase more expensive products than female consumers.

Average basket size, however, increases with age. For example, female baby boomers spent an average of $64.84 per transaction in January and February 2023, 22.2% larger than female Gen Z consumers.